TPS Superintendent Q&A Response

Detailed response to recent budget overestimation and closed door meeting

I recently covered the October 13th TPS school board meeting (linked here: October 13th Meeting Notes). A colleague of mine, Anthony Alaniz, wrote an article specifically covering the budget issue, which you can read here: Anthony Alaniz’s article. Over the weekend, TPS Superintendent Matt Hilton released a statement on the TPS Facebook page addressing these articles and issuing a Q & A, which you can read here: Mr. Hilton’s response, and Q&A.

For added clarity, I’ve uploaded the video of Mr. Hilton from the latest board meeting reminding folks that funds were not “lost”.

Mr. Hilton’s response to the word “blunder” and insistence on the need to present “the facts” seems to indicate his disagreement with the content of our articles. Neither article accused Mr. Hilton of any wrongdoing, but it is possible that he dealt with rumors stemming from the headline. I will let Mr. Alaniz defend his use of the word “blunder”, but will go on record as supporting it.

Let’s go through Mr. Hilton’s Q & A line by line.

As Superintendent, I am committed to transparency and open communication with our community about district finances. Recently, questions have been raised about a budget variance related to “student supports”. My intention is to provide clear, straightforward answers to help you understand what occurred, the current financial health of our district, and the steps we’re taking to strengthen our budgeting processes.

I have always complimented Mr. Hilton on being transparent with financial matters, as my previous articles show. Mr. Hilton’s intentions or commitment to transparency were never in question as far as I’m concerned. After all, if it weren’t for Mr. Hilton pushing back on Trustee Simpson, I wouldn’t have video clips to post in this article.

Q: What is the $750,000 budget issue I’ve been hearing about on social media?

A: The approximate $750,000 primarily funded special education services - legally mandated supports for students with disabilities outlined in their IEPs (Individualized Education Plans). This represents an overall 2% variance between what we budgeted and what we spent. It’s important to understand, contrary to social media rumors, that these funds were not lost or misspent; rather, this reflects an issue with our upfront budgeting process that we’re now addressing. Every dollar went to providing legally required services to students with disabilities.

Again, the issue is not how the money was spent, but rather how we estimated these costs in our budget.

In my meeting notes (previous article), I quoted, and agreed with Trustee Simpson that the $750k was not “lost”, but rather overestimated. To my knowledge, no one accused Mr. Hilton of misallocating these funds. Hilton describes this as a “variance”, and it is, but the word variance leads one to believe the problem is routine, which may not be the case. In the following clip, we hear Trustee Lewis mention that this situation has only happened one other time in his career.

Lewis describes this incident as, “bad news”, “(Hilton was) shy of spewing blood”, “lost sleep over it”, and “could go south in a hurry”. These are descriptors of a blunder, not a benign variance. At the very least, public concern is rational and warranted.

Here’s a quick explanation of our situation, provided by AI:

Understanding the Budget Variance: An overestimation of funds means your budget was based on an assumption of having $750,000 more than you actually have. Spending this amount on student services, while beneficial for students, implies that the funds were not available in your actual revenue or reserves, leading to a $750,000 deficit in your overall budget.

Impact on Other Areas: Since the $750,000 was spent on student services, that amount is no longer available for other budgeted areas (e.g., teacher salaries, facilities maintenance, transportation, or other operational costs). This creates a $750,000 shortage that you will need to address to balance the district’s budget, as school districts are generally required to maintain balanced budgets under state regulations (e.g., Michigan’s School Code).

This was an overestimation, not a “loss”, so it is entirely possible that we can continue to fund services with the money we do have (i.e. our savings account takes the hit, not our services). It is also possible that we will have to make cuts *somewhere* that we had hoped not to if our fund balance cannot cover the expenses. It is also possible that we pay for these expenses by further depleting our fund balance, which is concerning as I will detail further into this article.

Q: Did the district overspend its budget?

A: No, this is a common misconception. We under-budgeted for special education services, we did not overspend our overall budget. At the end of the year, we still added money to our fund balance (the district’s savings account). The more accurate way to describe this is that we put less into savings than we had planned, not that we overspent our budget. Another way to say it is this - we improved the district’s financial position, just not as much as we had planned.

To be clear – I’m not saying I’m happy about the inaccuracy in budgeting and the resulting variance. I’m not. And we will fix it moving forward. I just want to be crystal clear about the fact that we didn’t deficit spend in 2024-25.

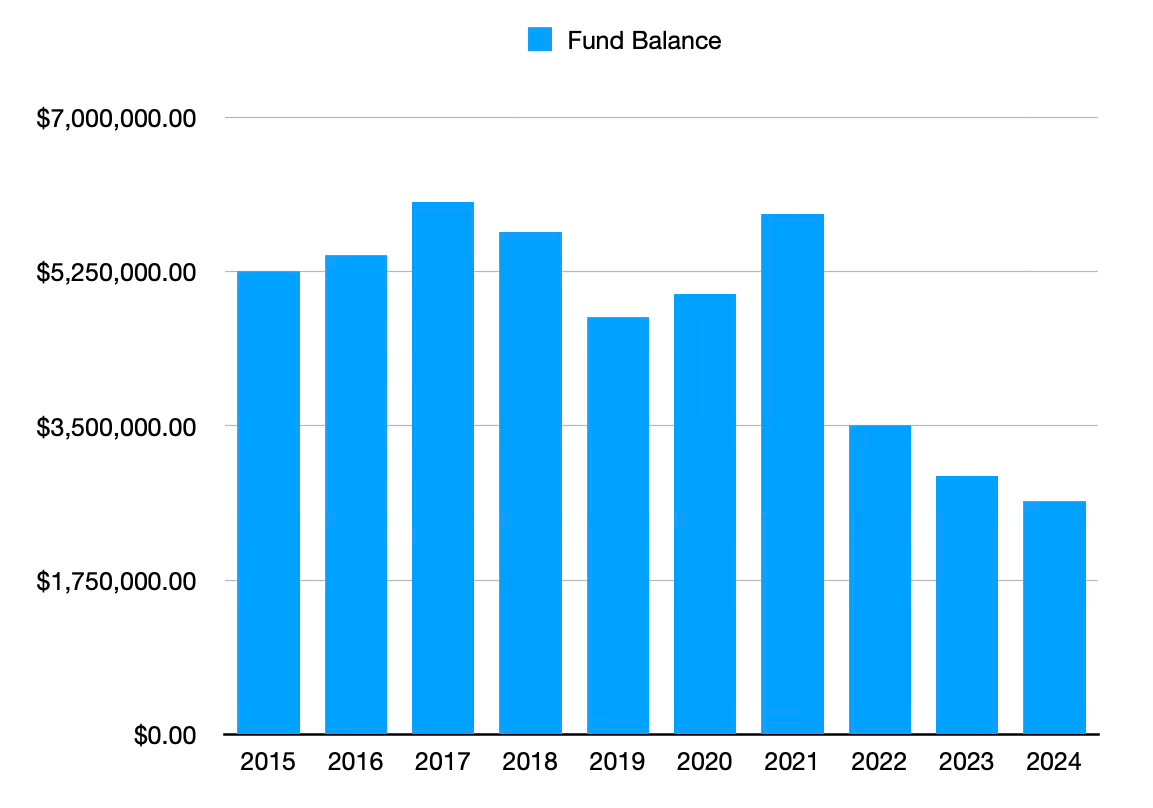

Mr. Hilton’s explanation here is spot-on, assuming this is true. It should be noted, however, that our fund balance has been steadily depleting since the 2018 recall, with exception made for an influx of COVID funds (2020-2021).

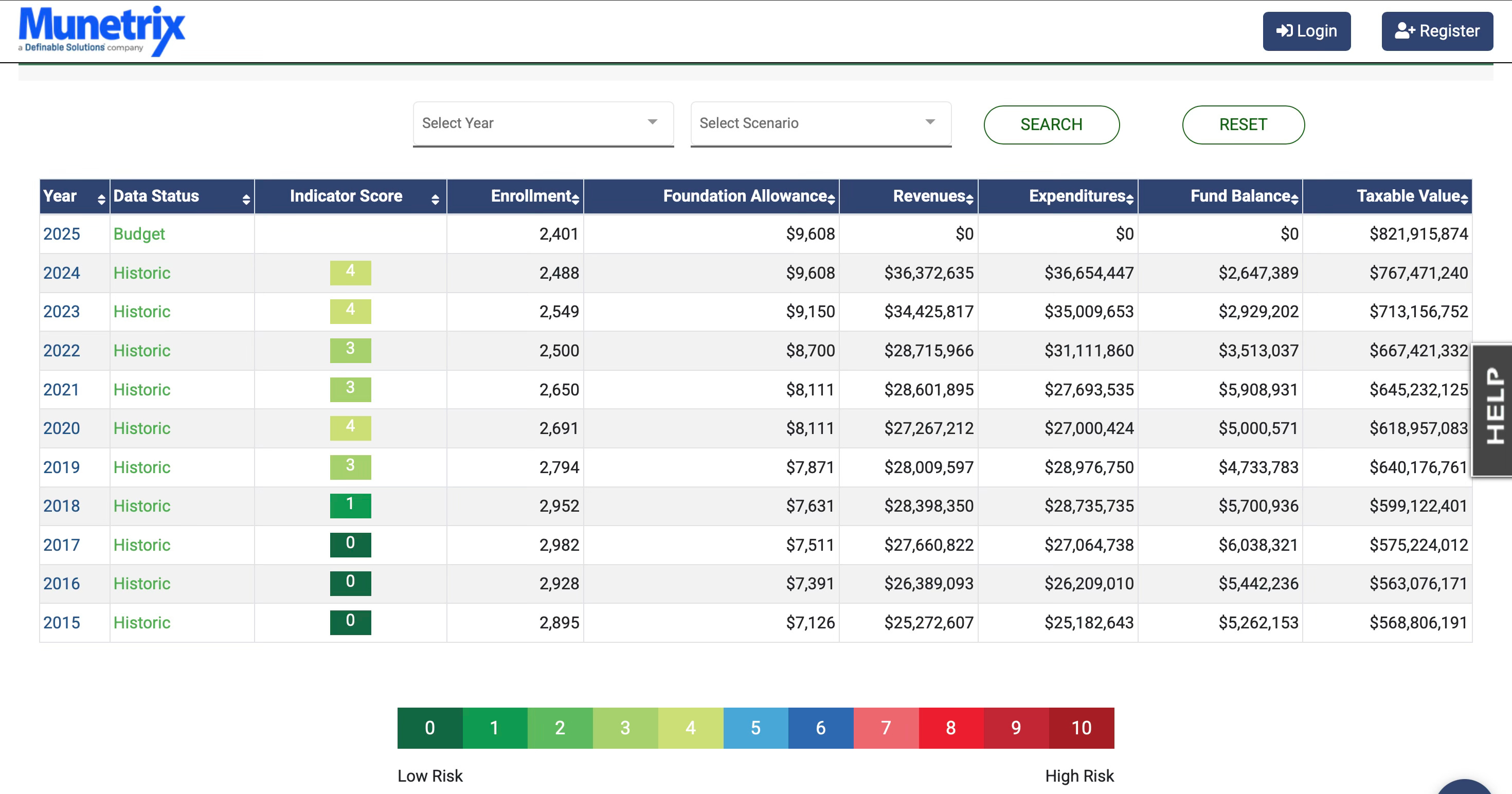

Source: Munitrix Data

I put this chart together a year ago using Munitrix data, which you can verify on their website. I even wrote an article last year concerning our funds levels, which you can read here: TPS Fund Equity Levels. We’re graded on our risk level, which *can* be seen as a financial responsibility level. Notice the risk level for our finances has been climbing since 2018. Some numbers for 2025 aren’t in yet. They usually come around mid-November. I’ve been waiting on this info to write my follow-up article with an updated year-to-year comparison. None of numbers on this chart or in my fund equity article reflect Hilton’s leadership. Many of these years were under former superintendent Rick Hilderley. It is entirely possible that Mr. Hilton will still right the ship this year.

The government shutdowns have hurt our district. In years past, we could weather these storms by having a strong fund balance or, as Mr. Hilton refers to it, a strong “savings account”. Our fund balance is now so low that we are required to take out loans to cover our expenses. We just approved a loan this month, though hopefully we will not have to use the loan (should state funds be released). I covered this in a previous article which you can read here: September 22 Meeting Notes.

Q: How was this variance discovered?

A: Our annual auditors recently identified a variance between our budgeted numbers and our actual audited numbers. This was brought to my attention by our former Director of Business Services.

In Lewis’s clip, we hear him saying, “Deb left”, and that Kelli’s absence was “unplanned”. At first, I assumed this blunder was Kelli’s fault since her departure was “unplanned”. There is a theory floating around social media that Kelli may have simply thrown in the towel. If Kelli was forthright in bringing this error to Mr. Hilton, and her counterpart also left recently, are the two connected? Are Deb and Kelli fleeing a hopeless situation? We recently lost a beloved principal in a sudden manner as well. High attrition levels all at once do tend to point to trouble. It’s fair to ask the question in absence of information made public.

Financial Safeguards and Improvements

Q: What is the district doing to prevent this from happening again?

A: We’ve implemented a comprehensive approach focused on both revenue and expenditure forecasting:

Revenue side: In the Spring of 2025 (well prior to the annual audit discovery), I directed that we take a conservative approach for estimating 2025-26 revenue for state funding and enrollment projections.

Expenditure side: Our new Interim Director of Business Services, Mr. Steve Lenar, is analyzing our 2024-25 actual expenses against our 2025-26 budget to ensure congruence. Mr. Lenar is also developing more robust monthly expenditure reports which will allow us to make timely adjustments, if needed.

To note: Mr. Lenar is a long time Michigan Schools Business Official having served multiple districts in Michigan as Chief Financial Officer and Assistant Superintendent of Finance. He brings a wealth of credibility, expertise and experience to Tecumseh. I want to thank him for jumping in on short notice.

I have some disagreements with how effective these changes will be, but I’ll save those for another article. Mr. Hilton is correct, he did recommend a conservative approach. If I recall correctly, Trustee Simpson recommended going even more conservative than the rest of the board in his estimates. He may have been right.

Q: What are monthly expenditure reports and how will they help?

A: These are detailed reports that track our projected budget against actual expenses and encumbrances (committed funds) on both a monthly and year-to-date basis. They include percentage checks to ensure we’re on track relative to where we should be at any given point in the school year. By implementing a more robust monthly monitoring system, we can identify and address issues much earlier.

This is important to note. I watched (and reported on) a meeting in which Trustee McGee was pushing for monthly statements. Ms. Glenn said it’s difficult given the nature of district finance, and she’s right, and I agreed with her at the time, but it is still possible. When McGee asked for this information, she seemed to get pushback from Trustee Brooks in the form of condescending comments, implying McGee was inexperienced. Admittedly, it was this pushback that made me suspicious of how much oversight we are providing as a district.

Q: How did the district approach revenue budgeting differently for 2025-26?

A: As mentioned earlier, we took a deliberately conservative approach. The budget planning process begins in January when the State of Michigan holds its first Revenue Estimating Conference. Even when the legislature projected increases of over $400 per student, we budgeted for only $250. This approach resulted in receiving more revenue than budgeted for 2025-26, a much better position to be in.

Agreed, and I reported this accordingly at the time.

Q: Is the district in financial trouble?

A: No. We added money to our fund balance in 2024-25. Due to our conservative budgeting approach for 2025-26, we’re projecting to receive more revenue, about $450,000.00, than we budgeted for. These factors position us well for growth and stability while we work to improve our budget processes.

“we’re projecting” $450,000. Does this projection use the same formula that told us we were receiving $750,000? It’s a fair question to ask.

Q: What is a fund balance and why does it matter?A: The fund balance is essentially the district’s savings account. It provides a financial cushion for unexpected expenses and helps maintain stability.

Agreed, it maintains stability.

Conclusion

To be clear, money was not lost, we did not deficit spend, we did not “rob” the savings account in any way for operating expenses – in fact, we added to it. This money was spent on our most vulnerable children. If someone wants to label that act as a “blunder”, I’ll live with that “blunder” every time.

Let me be absolutely direct: calling the funding of legally mandated services for students with disabilities a “blunder” fundamentally misrepresents both what occurred and what our obligations are as a school district.

These weren’t discretionary expenses. These weren’t frivolous purchases. These were services required by federal law for children with disabilities – services outlined in their Individualized Education Plans that we are legally, morally, and ethically bound to provide.

The characterization that I somehow made a “blunder” by ensuring these children received their legally mandated supports is not just inaccurate - it’s offensive to the families we serve and the values we hold as a community.

As I read these accusations, I don’t believe Mr. Hilton is responding to my article, or Mr. Alaniz’s article, as we never accused him of “losing” money, and certainly not of “robbing” anyone. My guess is that these were Facebook comments, or rumors within the district stemming from this headline.

Still, I’m disappointed that Mr. Hilton chose to reference our articles (using the word “blunder”), while responding to accusations that were not made in our articles. Had Mr. Hilton felt that my article was inaccurate in any way, he could have called me, as he has before, and advised. I’d have gladly posted a clarification where needed. I quoted both him and Trustee Simpson in my article. Perhaps he, like many others on Facebook, went off the headline without reading the actual article?

Here are the facts:

We did not overspend the budget. We under-budgeted in a particular area. At the end of the fiscal year, we added money to our fund balance. As a result, our district’s financial status improved.

No one doubts that putting money you thought you had into a savings account will improve your financial status. The question is whether we have enough to cover that amount when other expenses are factored in. It is possible that we didn’t need the $750,000 after all. Maybe, maybe not. We’ll find out soon.

Every dollar in question went exactly where it should have gone - to providing specialized instruction, therapies, accommodations, and supports for students with disabilities.

Again, I have every confidence that this is true, and said so in my article.

The issue is not the spending. The issue is improving our forecasting process so we more accurately predict these costs upfront. That’s exactly what we’re doing now.

We’re improving our processes. We’re implementing stronger safeguards. But we will never apologize for spending more to serve students with disabilities while, at the exact same time, staying within our overall budget and improving the fiscal health of the school district.

After all, the goal of any school district is not to make a profit or drive its fund balance up. Rather, it’s to spend its dollars in support of its children while maintaining or improving the fiscal health of the district each year. We did exactly that.

Sincerely,

Matt

No one is asking Mr. Hilton to apologize for spending money on student services. Again, perhaps some yahoo on Facebook threw out an accusation, but it’s beneath the dignity of Hilton’s office to respond to these comments if they are demonstrably false. We’re a smart bunch (at least my readers are), so we can tell the difference between an ignorant comment and a relevant question.

My Thoughts

Hanlon’s Razor

Hanlon’s Razor states: “Never attribute to malice what can more easily be attributed to incompetence”. I live by this. I don’t think anyone involved in this incident did so willfully. However, a director lost her job (or quit due to the incident). It’s fair that Mr. Hilton is facing the issue head-on. It’s also fair that taxpayers ask what’s being done to prevent this from happening again. Had he published this Q & A when the issue was discovered, not as a personal response to two bloggers, he likely would have avoided the pitchforks.

The Pitchforks

I left the nosey asses group on Facebook months ago because it was so toxic. I rejoined recently because I wanted to shine a light on how board members did not vote unanimously to discuss this incident behind closed doors. I felt it needed more attention. I took the risk that the pitchforks would come out, so I was extra careful to quote Trustee Simpson’s clarification that:

no money was “lost”

funds were spent on student services and added to our fund

(Trustee Simpson’s comments)

Public anger isn’t inherently bad. It gets things done. It has saved careers in this district. I try to inspire folks to educate themselves on the issues before taking to the comments. It’s why I created this blog. If the district would publish information packets before meetings, like every other district (and our city council) already does, there would be no need for bloggers like me.

Closed Doors

I’ve uploaded the vote to go behind closed doors, and the statute used.

The following is the statue quoted:

(h) To consider material exempt from discussion or disclosure by state or federal statute.

The following is a summary of the Open Meetings Act:

Public Act 267, Michigan’s Open Meetings Act, allows public bodies to go into a closed session for specific, limited purposes, such as personnel matters, collective bargaining, and legal consultations. A closed session requires a two-thirds roll call vote of the members and must be preceded by a public vote with the reason for the session stated in the minutes. Decisions must still be made in an open session.

(provided by Google AI)

I added an update in my last article, which I will post here:

I was informed by a friend of mine with knowledge of these matters that the board likely went into closed session to discuss an opinion written by their attorney. This matter would be covered by attorney-client privilege, and would warrant a closed session. That being said, it is also possible for the board to have waived this privilege and held the meeting in public. Additionally, discussion of where the $750,000 was spent could also have been made public.

(article linked in top paragraph)

At the end of this closed session, the board votes to appoint an interim director of business services, implying Kelli was no longer our director.

If the board went behind closed doors to discuss things with an attorney, is this the same attorney that determined former Principal Niles’s alleged sexual misbehavior with students was merely “non-sexual touching”, giving him a severance package of $80k and transferring him to be a pool director (details here)? If so, is it really a surprise that the public is interested in what was being discussed?

Was a decision made? If so, why was it not discussed in open session?

If Kelli left of her own volition, why were they in closed session as there was no disciplinary action?

Why did Trustees McGee and Miller seem to think the meeting should be held in public?

These are the questions I had when I wrote my article. They have nothing to do with Mr. Hilton and everything to do with more of the same from incumbent board members and the usual administrative staff involved in prior scandals. I ask these questions because no one else is asking. I ask these questions because members of this community insist that I ask. I’m interested in answers, not scandals. Perhaps there’s a perfectly good reason for it all. Great! What’s the reason?

Mr. Hilton

Anyone who’s known me since the election knows that I’ve essentially been Mr. Hilton’s cheerleader since the beginning. I attended his interview with the board. It was the best interview I’ve ever seen, bar none. I found him to be honest, sincere, and a “culture person”, like me. I wrote him the day he got the job to say I’d support him however I could. Since then, I’ve continually spoken out in favor of his leadership. I liked what I was saw, but my faith is now beginning to wane.

Tecumseh has had a string of scandals since the 2018 recall, which MLive documented in this article. None of these scandals happened under Mr. Hilton’s leadership, but they did under some of our current board members. There’s reason for folks to be skeptical of the administration as a whole, and this should not be taken personally. I can accept that Mr. Hilton was trying to prevent mass panic, but I find his “it’s fine” assessment to be overly optimistic at least, and misleading at worst.

I will continue to write this blog with contributions from folks within this community for as long as it takes this district to get this information out on their own in a timely manner. Mr. Hilton’s administration is more than welcome to reach out to me if they feel anything in my articles are in error or a misrepresentation. In the end, we’re all on the same side: more transparency.

Additional Reading

The following is the latest article I wrote containing budget updates: June 23 Meeting Notes